So You Just Received Some Stock Options...

I love startups. The environment is far more dynamic at small companies than at large ones. Decisions get made quicker because they have to be. Every startup is born on life support. I'm the sort of person that needs to keep moving and startups let me do that. I've actually been told at some jobs to sit tight while waiting for more work to come up. That's never happened at a startup.

I won't pretend that I also don't enjoy the excitement of a potentially large payout. I definitely do. The challenge is understanding what that payout is. Not every startup is going to give you the chance of making retirement money. The enormous number of millionaires minted by the Google and Facebook IPOs is a situation that is as rare as companies like Google and Facebook.

If you're curious about how to understand a potential offer from a startup, have no fear! I'm about to explain it with all the confidence of someone who did a couple of internships on Wall Street. Like a lot of financial posts out there, I have to tell you that I am not a registered financial advisor. This post is for informational purposes only and is not intended as, and shall not be understood or construed as, financial advice. You're responsible for your own choices. With that out of the way...

To understand how startup valuations work, we should start with the basics: markets. Think of your local grocery store. If they set the price of apples too high, then people will not buy them. The options are to lower the price (and accept lower margins) or not sell apples. If they set the price too low, they run out of apples because people will end up buying all of them since it’s a good deal.

The question then becomes, how do grocery stores set the appropriate price for an apple? What is the most you would pay for an apple? Do you think it is the same as your neighbor? Or your coworker? Or your parents? Probably not. Everyone has a different value that they would place on the same good or service. Providers of goods and services have to make the best guess they can. Maybe they use some mathematical formula to make themselves feel better about their decision, but it ultimately is still a guess at the end. It may be an educated guess, but it's still a guess. They have to go to market with a price and hope it works out. If it doesn't, they now have data needed to adjust.

There's no magic formula for prices. A price is not a fact. It is an opinion and everyone has a different opinion. The price of anything is the convergence of the opinions of the majority of sellers with the opinions of the majority of buyers.

A grocery store may say an apple costs $20 each, but that alone does not set the price. If no one buys a $20 apple, then they will either have to lower the price explicitly or through discounts/coupons. It is only when the listed price goes down to a level where people are willing to buy that apple does the real price get set.

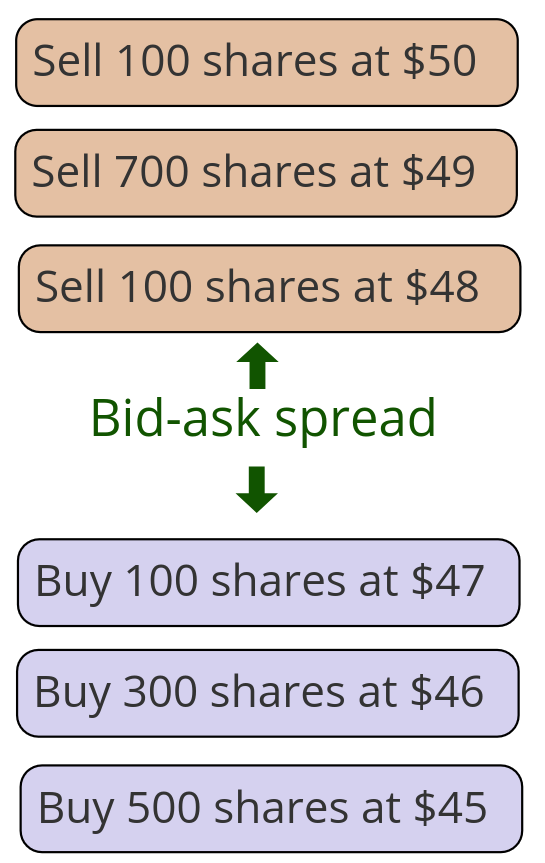

With that understanding, let's move to stocks. I made a very very long introduction to the stock market here, but I'm going to summarize it significantly. The way markets work is people define how much they are willing to buy or sell at a certain price by telling a stock exchange. Everyone sets a different price. The result is that there is going to be a price that is the highest a potential buyer is willing to buy at and a price that is the lowest a potential seller is willing to sell at. The difference in these two prices is called the bid-ask spread (buyers are bidding, sellers are asking).

This difference always exists. The reason it always exists is because exchanges are mostly automated these days and as soon as there is an overlap, a stock trade happens. The buyer and seller have agreed to a price and execute the trade. The result is a new bid-ask spread.

How do people come up with these prices though? What helps people make a decision? Every stock trader is going to have their own formula or technique, but it ultimately is the same as our market for apples: everyone is guessing. Determining a price is not an exact science. Stock prices would not fluctuate the way they do if it was. The stock price would change 4 times a year when financials are released if setting prices was an exact science. A lot of stocks have a price change more than 4 times a second. There's no deep scientific analysis in a quarter of a second.

Part of the reason that everyone is guessing is that you can't just look at the financials. A company making $1 billion a year with a 50% margin and $3 billion in the bank may look like a business worth $10-$20 billion. But what if that business was selling beepers in 2005? Do you even know what a beeper is?

The value of a business isn't just the financials. Financials are important, but they represent the past. The value in a business lies in the future, of which the past is only one indicator of many. Accounting for all indicators would give you the intrinsic value of a business, but intrinsic value can only ever be an estimate. If predicting the future was an exact science... we'd all be very very happy. Even Warren Buffett and Charlie Munger, two of the greatest investors of all time, came up with different estimates for the value of businesses.

There's a famous quote from Benjamin Graham where the stock market is a voting machine in the short term and a weighing machine in the long term. I'd argue that the stock market is always a voting machine. But much like a broken watch is right twice a day, people eventually vote for a stock price that someone like Benjamin Graham or Warren Buffett would also vote for.

Now that we've established that everyone is at best making an educated guess when determining prices, let's cover one more thing before we move to startups: market capitalization.

The last trade conducted sets the valuation of the entire company. It does not matter that 100 shares out of 1 billion total were in the trade. The stock price is always set to whatever the last trade was. The market capitalization is simply the stock price multplied by the total number of shares.

The implication here is very very important. If a company has 1 billion shares and it's stock price is $10, it is worth $10 billion. If the *very* next trade sets the stock price to $20, the company is now worth $20 billion.

Where did that extra $10 billion come from? Did the government just print $10 billion when the stock price was set?

Consequently, if the stock price goes back down to $10, did we just set $10 billion in crisp benjamins on fire?

Obviously not. The market capitalization does not actually represent money available. All it represents is the last trade. If you owned a large amount of shares, you couldn't even sell them all for that price. You'd have to go down the list of buyers and sell for progressively less. Going down the list of buyers to lower prices would also lower the stock price, which people use as an indicator, so the potential buyers would set their prices even lower.

This is why a lot of wealth is called "paper" wealth. You have that much money on paper, but things would be different if you tried to turn that paper into money you could spend.

Finally, we come to startup valuations. Startup valuations are just like market capitalizations, the difference being there are significantly fewer trades. If you include the seed round, a Series C company has had 4 trades in its lifetime (seed round + series A + B + C). Compare that once again to say Coca Cola which could have more than 4 trades a second.

If a startup raises $100 million by giving the investors 20% equity, that startup is valued at $500 million. It does not have access to $500 million in cash. It only has $100 million to spend. The other $400 million exists only on paper. The investors and the founders agree that it exists, but it can't be spent.

Whereas a public company like Coca Cola has years if not decades of financial history for you to look at, a startup has only promises of the future. The intrinsic value is signficantly harder to calculate without history. With fewer trades, there are fewer investors and far less scrutiny. The odds of any of those investors making a mistake is significantly higher than the average stock market participant and that results in higher fluctuations. WeWork was valued at $47 billion at the beginning of 2019. It was valued at less than $3 billion in 2020 after only 2-3 trades. Coca Cola would go from being worth $310 billion to $310.2 billion in 2-3 trades.

Money doesn't just appear or disappear. What's changing is not how much money is available, but how much people think a company is worth. Like stock markets, there's a list of people willing to buy at a certain price and people willing to sell at a certain price. The list is just a lot less clear with a startup than a public company. No stock exchange is automating the trade either. It's a lot of negotiation and setting terms in a contract. This means that when you get equity, you can't just sell it to anyone. You have to wait until the company becomes public or someone has the actual cash to buy the company outright (or a secondary, but that's rare). What the company will be valued at when that happens can be vastly different from valuation in the last fundraising round (hopefully higher if I have equity). A payout from startup equity is really determining the future intrinsic value of the business. If the current instrinsic value is what people think the future will bring for the business, then determining the expected payout from startup equity is thinking about how people in the future will think of the future. The calculation is incredibly nebulous.

There's also a lot that can go into the calculation for current intrinsic value. Does the business make sense? Is the product good? Are the investors an asset? Are the founders going to be able to execute well? A lot of questions can be asked, but unfortunately none of the answers can be determined with exact science. If someone wanted you to work for their beeper startup in 2005, you would have probably thought they were crazy. There was no deterministic way to tell that they were crazy, but you would have been making an educated guess based on your knowledge of the world that making beepers is a terrible idea. The same goes for any investor no matter what they say. There may be some numbers to back up a decision, but in the end an investment is an intuitive decision. As someone who is willing to work for a lower salary in exchange for equity, every startup employee is effectively an investor and has to think like an investor to understand what that equity is worth. That means building up an intuition about businesses and making your own determination about the value of the startup.

By the way, if anyone reading this has been thinking "I know a really successful beeper startup" the whole time, please let me know. I'm generally interested to know how they made it work.

There's also a lot to be said about how options and taxes work (lots of people in the US learn about AMT the hard way). Those are topics for another time.